Long-lived and short-lived greenhouse gases have been the subject of debate in New Zealand for some time. Understanding how they contribute to climate change is particularly important now the Government is considering a new emissions target for 2050. There are three options on the table:

- Net zero carbon dioxide

- Net zero long-lived gases and stabilised short-lived gases

- Net zero emissions across all greenhouse gases

This would replace the current target to cut emissions to 50% below 1990 levels by 2050.1

Which target?

The first target should be dismissed because it ignores other long-lived gases, including nitrous oxide, which accounts for over 10% of New Zealand’s emissions. Nitrous oxide lasts for over 120 years in the atmosphere. It has a warming effect that is more than 250 times that of carbon dioxide over a 100-year timespan.2

New Zealand’s nitrous oxide emissions have also been rising steadily since the 1990s as farming has expanded and intensified. These emissions stem from livestock urine and dung, and fertilisers. Cutting nitrous oxide emissions has the co-benefit of improving the health of our waterways, which have become heavily polluted by nitrate runoff from farms.3

This leaves us with the second and third targets, which is where it gets complicated. Should we cut all greenhouse gases to net zero? What is a long-lived and short-lived gas? And what does ‘net zero’ mean anyway?

Long versus short-lived greenhouse gases

Long-lived gases, including carbon dioxide and nitrous oxide, accumulate in the atmosphere. The total stock of historic emissions has locked in a degree of global warming that cannot be reversed. Ongoing long-lived emissions will continue to warm the climate.

Average global temperatures are now more than 1°C above pre-industrial levels.4 The only way to avoid the 2°C increase in global temperatures that we committed to under the 2015 Paris Agreement is to cut long-lived emissions to net zero. Both the second and third proposed targets take this into account.

Net zero implies that persistent long-lived emissions are offset, either by planting forests that absorb carbon dioxide or purchasing overseas ‘emissions credits’. The latter could, for example, serve to discourage deforestation abroad rather than planting more trees in New Zealand.

Short-lived gases also contribute to global warming, but the flow of emissions rather than the total stock in the atmosphere is what counts. This is because short-lived gases break down and exit the atmosphere faster. For example, methane is a short-lived greenhouse gas with an average atmospheric lifespan of just over 12 years.2 In New Zealand, methane from cattle and sheep makeup over 40% of our total emissions.3 Outside of New Zealand, methane is primarily emitted during oil and gas production, as well as equipment and pipeline leaks.

If atmospheric inflows of methane are equal to outflows then its contribution to global warming is fixed and, unlike long-lived gases, this does not worsen over time. Of course, this still implies some ‘warming’, even if it is not rising. This is the approach proposed for the second target.

Stabilising methane

It could seem fair to say that the New Zealand agricultural sector, which is responsible for the majority of methane emissions, should be allowed to continue emitting as long as it’s not making global warming any worse. However, implementing the second target is still likely to involve reducing methane emissions to shrink their overall contribution to climate change. This begs the question: how much methane-induced warming should be allowed? Or, at what level should we stabilise short-lived emissions?

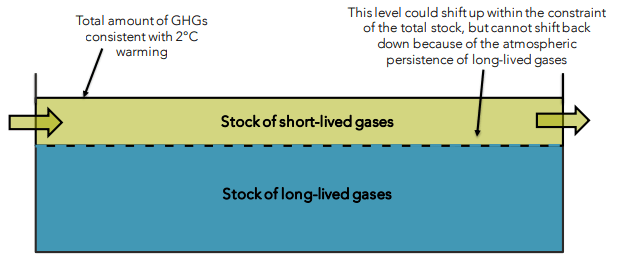

The answer depends on our emissions budget ⎼ the amount that we can still emit in New Zealand, and globally, before breaching the 2°C temperature threshold agreed in Paris. The more long-lived gases we emit, the more we eat into our short-lived gases allowance. This is illustrated by the Productivity Commission’s diagram below:3

The second target leaves room for different interpretations of the appropriate stabilisation level. Once it is set up, the new Climate Change Commission will be able to advise on this. Depending on final wording of the second target, successive governments might be able to adjust the level. This could give us some flexibility in achieving our 2050 target, but would also result in some uncertainty for households and businesses. Since the chosen target is likely to remain in law until 2050 we ought to minimise ambiguity.

Warming decelerator

Deploying methane as a global warming ‘decelerator’ is the approach proposed for the third target. If outflows of short-lived gases exceed their flow into the atmosphere, this can actually counteract some of the warming being driven by historic long-lived emissions. If we cut methane emissions to net zero, their contribution to global warming will also reach zero within a few decades. The same cannot be said of long-lived carbon dioxide or nitrous oxide emissions.

The Paris Agreement requires us to “pursu(e) efforts to limit the temperature increase to 1.5°C”. This is a more aspirational target than 2°C, but the Agreement recognises this as the safer limit that “would significantly reduce the risks and impacts of climate change.”5 To have a high likelihood of limiting warming to 1.5°C, we need to limit the atmospheric concentration of greenhouse gases to 350 parts per million.6 But we exceeded this limit in 1988.7 The probability that warming is limited to just 1.5°C has been in steady decline ever since.

As the world continues to emit long-lived gases, cutting methane emissions can delay the arrival of the 1.5°C temperature limit. According to a leaked special report from the UN Intergovernmental Panel on Climate Change, this is expected to happen in 2040.8 Net zero methane would also dramatically improve our chances of avoiding warming of 2°C. Just as importantly, it might see us avoid climate tipping points, like the collapse of the Gulf Stream or the melting of the Arctic permafrost ⎼ events that cannot be reversed.

Methane has a warming effect over 80 times stronger than carbon dioxide over a 20-year period.2 This effect does not last forever, but the next few decades are crucial because we have already run up a debt. Cutting methane emissions to net zero is like selling your car to meet your mortgage repayments and avoid foreclosure.

Our climate, your say

It is difficult to conclude whether the second or third target is best. Both are grounded in science and make sense.

Should New Zealand cattle, sheep and dairy farmers cut exports and innovate their way to net zero? Industry, as well as the energy and waste sectors that produce long-lived emissions, certainly must.

New Zealand will not remain unaffected by sea level rises, extreme weather events, drought and wildfires, or an increase in airborne diseases and the other effects of climate change. Yet, we know that developing countries will bear the brunt of this. Should New Zealand cut all emissions to net zero by 2050, so our neighbours in the low-lying coral atolls in the Pacific have the best chance of preserving their homes?

The choice is ultimately a moral one, even cosmopolitan, as it asks us to consider the benefits to people beyond our borders.

You can make a submission here: Our Climate. Your Say.

Footnotes:

[1] New Zealand 2050 target, Ministry for the Environment

[2] Global Warming Potential, IPCC Working Group 1, Assessment Report 5, Chapter 8, Table 8.7

[3] Low-emissions economy, Productivity Commission

[4] Climate Monitoring, US National Oceanic and Atmospheric Administration

[5] The Paris Agreement, UNFCCC

[6] Radiative Forcing Stabilisation Level, IPCC Working Group 2, Assessment Report 4, Chapter 19, Figure 19.1

[7] Atmospheric carbon dioxide, US National Oceanic and Atmospheric Administration

[8] IPCC Final Draft Report, Reuters

Further reading:

New Zealand Agricultural Greenhouse Gas Research Centre

NZ Climate Change Research Institute, Victoria University