My last post explained why international oil prices have fallen dramatically during the last six months. This has harmed the profitability of many oil producers.

International oil traders and producing companies have called on the Organisation of Petroleum Exporting Countries (OPEC) to react to the fall in oil prices. Saudi Arabia is the biggest producing country within OPEC and often represents the group. But what can the Saudis do?

For a long time Saudi Arabia was the world’s largest oil producer. The shale oil revolution changed this. Last year, we saw the US overtake both Saudi Arabia and Russia – the other big player – to become the world’s largest oil producer. Nevertheless, the US consumes a lot of what it produces. Saudi Arabia is still the world’s biggest exporter. Moreover, its vast reserves and production capacity allow it to “swing” supplies. That is, quickly alter the volume of oil it puts into the international market. In a nutshell, decreasing copious OPEC supplies would alleviate the international supply-glut and boost the international oil price.

To do this OPEC must accept a decrease in total sales volumes and a smaller market share. The burden of cutting back volumes falls predominantly on Saudi Arabia as OPEC’s biggest producer. Saudi Arabia has had experience in the past with cutting supplies whilst other OPEC members “free ride.” Meaning they benefit from an increase in prices without decreasing their sales volumes as agreed.[1]

International producers are effectively asking Saudi Arabia to do them the same favour. Just why would it do so in a competitive market?

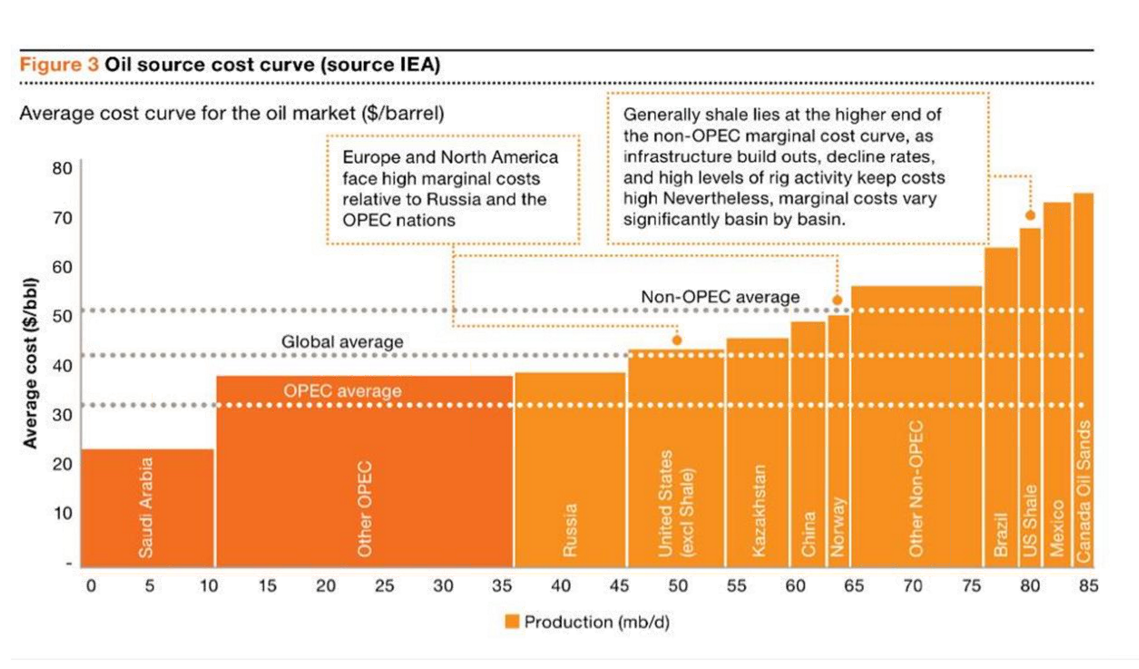

For the moment Saudi Arabia has indeed refused to offer anyone any favours. What’s more getting oil out of the ground is very cheap in Saudi Arabia. Its oil wells have some of the lowest “lifting” or production costs in the world. This is what the graph below shows us:

The ultra-polluting Canadian tar sands projects are well out-of-the-money at oil prices of $50/barrel, since it costs $85 to produce a barrel of oil.[2]

The graph also shows us that Saudi Arabia can remain profitable close to $20/barrel. It could let current prices keep falling without sacrificing market share. Today’s oil price is less of a problem for Saudi Arabia than other countries where lifting costs are higher.

Yet, it is unlikely Saudi Arabia will let prices fall that far. Profits from oil sales directly support the Saudi government’s budget. Also, higher prices eventually become more important than sales volumes as profit margins tighten. For example, if I sell ten barrels at $100 each this is the same as selling a hundred at $10 each. Except that if it cost me $9 to produce each barrel my total profit is $910 in the first scenario and only $100 in the second scenario.

For now Saudi Arabia appears content to keep the price low and wait for US shale oil producers with thinning profit margins to leave the market. This strategy will cause the US shale oil revolution to lose pace and protect Saudi Arabia’s market share in the long term. However, we might see OPEC revise their policy later in 2015.

[1] It’s hard to measure exact output and countries report their own production volumes.

[2] I’ll write about the economic feasibility of the tar sands projects soon.